Construction sector’s subdued start to year continues

UK construction companies indicated a sustained downturn in business activity, alongside pressure on margins from sharply rising input costs.

Combined with a drop in new orders, this contributed to the fastest reduction in employment numbers for nearly four-and-a-half years.

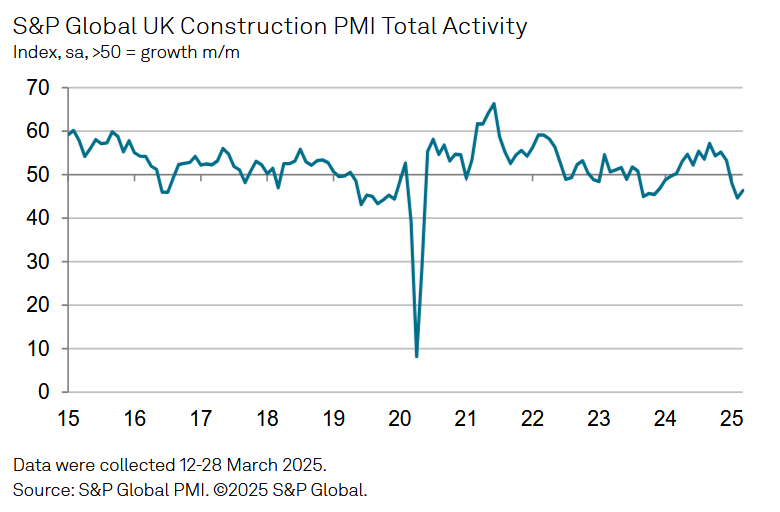

The headline S&P Global UK Construction Purchasing Managers’ Index™ (PMI®) – a seasonally adjusted index tracking changes in total industry activity – posted 46.4 in March, up from a 57-month low of 44.6 in February but still well below the neutral 50.0 threshold. Lower volumes of construction output have now been recorded for three consecutive months and the latest reading indicated a solid pace of contraction.

Civil engineering (index at 38.8) was the weakest-performing area of activity in March. The sharp decline in output levels was attributed to delayed decision-making on new projects and a generally subdued pipeline of major infrastructure work. The rate of contraction accelerated to its fastest since October 2020.

Residential construction activity declined at a slower pace than in February, but the respective seasonally adjusted index was still well inside negative territory (44.7). Survey respondents typically commented on weak demand conditions, although some suggested that easing borrowing costs had helped to support confidence.

Commercial building (47.4) deceased only moderately in March. That said, the rate of contraction was the fastest since January 2021. Lower business activity was linked to lacklustre UK economic prospects and the impact of rising geopolitical uncertainty on clients’ investment spending.

Sluggish demand conditions contributed to another marked deterioration in construction order books. Lower levels of incoming new work have been recorded throughout 2025 to date. Construction companies often noted a lack of sales enquiries and greater competition for new work.

Lower workloads, elevated interest rates and worries about the broader economic outlook continued to weigh on business activity expectations in March. Confidence across the construction sector slipped to its lowest since October 2023.

Some firms nonetheless noted positive sentiment regarding the outlook for demand across the renewable energy sector and hopes of a turnaround in infrastructure workloads. Mirroring the trends for output and new work, latest survey data indicated a reduction in staffing numbers for the third consecutive month. The rate of job shedding was the steepest since October 2020. Subcontractor usage also decreased at a solid pace in March, while construction companies reported further cutbacks to their input buying in response to lower workloads.

Finally, higher payroll costs due to forthcoming rises in National Insurance contributions and the National Minimum Wage continued to push up average cost burdens. The overall rate of input price inflation accelerated to its strongest since January 2023.

Tim Moore, economics director at S&P Global Market Intelligence, said: “March data highlighted a challenging month for UK construction companies as sharply reduced order volumes continued to weigh on overall workloads. Civil engineering experienced the biggest setback as activity decreased to the greatest extent since October 2020. Survey respondents commented on subdued sales pipelines and a subsequent lack of infrastructure work to replace completed projects.

“Commercial work also saw a headwind from delayed decision-making on major projects, largely due to worries about the impact of rising global economic uncertainty. The downturn in residential construction activity nonetheless eased since February, providing a source of encouragement despite ongoing reports of sluggish demand conditions.

“Construction companies remained cautious about their year ahead growth prospects, as fewer sales conversions and a third successive monthly reduction in total new work hit confidence levels. Overall business optimism slipped to its lowest since October 2023.

“A lack of new projects, alongside pressure on margins from rising payroll costs, led to hiring freezes and the non-replacement of departing staff in March. The net result was the fastest pace of job shedding across the construction sector for nearly four-and-a-half years.”

Neil Morey, technical director at Thomas & Adamson, part of Egis Group, said: “The challenges facing the construction sector continue to be reflected in the PMI data, with a mixture of global geopolitical uncertainty and limited economic growth in the UK continuing to affect the sector. While the weakening picture was balanced by a sense of optimism for future growth in previous months, it’s concerning that confidence has begun to take a turn too.

“Despite the gloomy backdrop, there are some bright spots. The commercial sector remains resilient, demand from the renewables sector is picking up pace – particularly in Scotland – and infrastructure spending could prove a catalyst for later in the year. More widely, sluggish economic growth could also prompt further cuts to interest rates, which would help unlock projects that have struggled to get off the ground due to financing costs.

“The current negative trajectory could well remain for a couple more months, but provided planned investment in infrastructure, housing, and the energy transition are made soon there are still reasons to retain optimism longer term.”

Brian Smith, head of cost management and commercial at AECOM, added: “Three consecutive months of falling output have deepened concerns across the sector, with continued contraction testing confidence among clients and contractors.

“The recent Spring Statement reaffirmed the government’s commitment to infrastructure – including a £13bn capital investment package covering key areas such as housing and defence. With a more stable investment climate, this points to potentially better months ahead and we hope to see this momentum maintained through the upcoming spending review. A cut in the interest rate in May would help unlock greater confidence among clients and investors to proceed with projects that had been on hold, although we probably need to see a fall in inflation first.

“Workforce pressures remain one of the biggest barriers to delivery. While the Chancellor’s £600m investment in construction skills is a welcome start, a broader strategy is needed to close the gap and ensure Britain has the capacity to build at scale. The private sector stands ready to work with government to turn planned investments into tangible delivery, supporting the UK’s long-term growth agenda.”

Malcolm Jackson, interim director of the Institution of Civil Engineers Scotland, said: “The latest S&P Global UK Construction Purchasing Managers’ Index noted civil engineering was the weakest-performing area of activity in March due to delayed decision-making on new projects and a generally subdued pipeline of major infrastructure work.

“The ICE has over 8,500 members in Scotland who design, build and maintain our vital transport, water, flooding, energy and waste infrastructure without which our communities could not function.

“We will continue to work with the Scottish Government to ensure infrastructure has the investment it needs to improve places, productivity, health and wellbeing.”