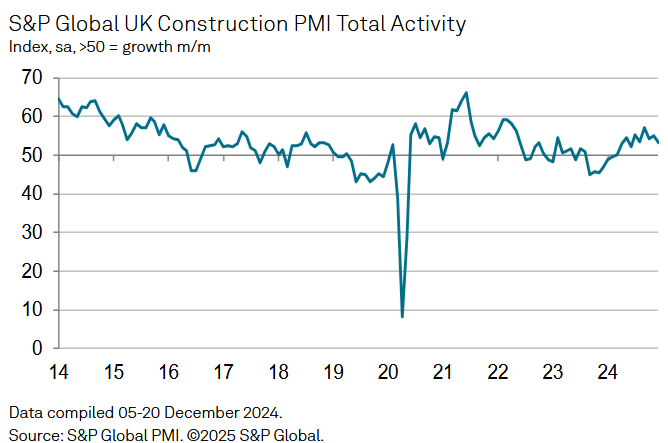

Output growth eases to six-month low

UK construction companies indicated a loss of momentum at the end of 2024, according to the latest figures from the S&P Global UK Construction Purchasing Managers’ Index (PMI).

Total business activity expanded at the slowest pace since last June, while new order growth moderated for the third month running. The headline PMI registered 53.3 in December, down from 55.2 in November and the lowest for six months. That said, the index has posed above the crucial 50.0 no-change value since March 2024 and the latest reading still signalled a solid upturn in overall construction output.

Commercial activity was the fastest-growing area of the construction sector in December (index at 55.0), followed by civil engineering (52.9). That said, both categories saw a

slowdown in the rate of business activity expansion since November.

Residential work was again the only category to register an overall decline in output during December (47.6). House building activity has now decreased for three consecutive

months and the latest reduction was the fastest since June 2024. Survey respondents noted that subdued demand conditions, elevated borrowing costs and weak consumer

confidence had all weighed on activity.

Mirroring the trend for output volumes, total new work also expanded at the slowest rate since last June. Anecdotal evidence suggested that improving tender opportunities in the commercial building sector had been offset by cutbacks to residential development projects and a lack of new business to replace completed infrastructure work.

Construction companies responded to weaker new order growth by reducing their input buying for the first time in eight months. In some instances, lower levels of purchasing activity were linked to tighter inventory management. Suppliers’ delivery times were broadly unchanged in December. While some firms noted improving vendor performance due to lower demand, there were also reports that shipping delays had led to longer lead times for imported items.

December data highlighted a decline in sub-contractor usage for the fourth time in the past five months. Despite lower demand for their services, sub-contractor availability

improved only marginally and at the slowest pace since March 2023.

Meanwhile, latest data indicated the fastest rise in rates charged by sub-contractors for 20 months. Adding to upward pressure on input costs, purchase prices increased at a

robust pace that was only slightly softer than November’s one-and-a-half-year high. Elevated cost inflation and rising salary payments were again cited as factors holding back staff hiring. The pace of job creation remained lower than the pre-pandemic average.

Looking ahead, around 48% of the survey panel predict a rise in output over the course of 2025, while only 15% forecast a decline. The degree of positive sentiment picked up sharply since November, but it was still much weaker than seen in the first half of 2024. While construction firms typically commented on optimism linked to long-term business

expansion plans, many also cited worries about the general UK economic outlook and tighter budgets for capital spending.

Tim Moore, economics director at S&P Global Market Intelligence, said: “December data highlighted a loss of momentum for construction output growth, with all three main

categories of activity posting weaker performances than in the previous month. Commercial building maintained its position as the fastest-growing area of construction

activity, followed by civil engineering. In contrast, residential work decreased for the third month running and at the fastest pace since June 2024.

“The slowdown in overall construction output growth reflected more subdued demand conditions in recent months, as illustrated by a further moderation in new order growth during December. Survey respondents commented on headwinds from elevated borrowing costs and the impact of fragile consumer confidence.

“Staff hiring picked up since November, but there were signs of tight supply conditions. Sub-contractor availability improved to the smallest extent since March 2023, while the rates they charged increased at the fastest pace for just over one-and-a-half years.

“Concerns about the demand outlook weighed on construction sector growth expectations for 2025. Although confidence recovered after a post-Budget slump during November, it was still much weaker than in the first half of 2024. Many firms reported worries about cutbacks to capital spending and gloomy projections for the UK economy.”

Jordan Smith, technical director at Thomas & Adamson, part of Egis Group, said: “The mixed set of indicators we saw in November’s PMI update continued into December, with activity moderating as 2024 came to an end. Housebuilding remains the laggard, which looks unlikely to change any time soon given the challenging backdrop in terms of interest rates and consumer confidence. That said, further detail around the government’s spending plans in the first half of this year could provide a boost to the sector in the not-too-distant future.

“Commercial and civil engineering work remains in positive territory, which reflects what we are seeing on the ground – even if it has weakened compared to a few months prior. We have seen a number of commercial refurbishment and retrofit schemes move forward across the UK and expect that to continue as 2025 progresses. Overall, while December’s figures are a mixed bag, there is still a good degree of optimism in the industry, and we have a significant amount of our 2025 workload secured as we move into the year ahead.”

Brian Smith, head of cost management at AECOM, added: “Despite output growth easing to a six-month low, the construction industry has still finished 2024 on solid footing.

“As we enter the new year, the positivity around sentiment in the last half of 2024 should result in growth in construction output in 2025. Contractors are encouraged but will want to see how the government’s plans – including changes to NPPF, increases in capital spending and a revised industrial strategy – can support the industry.

“The outlook looks brighter than this time last year but there remain challenges, with interest rates expected remain higher for longer, the malaise in the wider economy, changes to safety building regulations and persistent skills shortages that contractors need to solve whilst maintaining delivery.”

Brendan Sharkey, real estate and construction specialist at accountants MHA, said: “The fall in construction PMI is hardly surprising as the industry continues to benefit from the government’s investment in infrastructure but at the same time is hampered by still historically high interest rates and an uptick in employment costs.

“Activity in the commercial sector remains strong, but housing has dipped. Whether the housing market will see a reversal in fortunes this year remains to be seen, however the opportunity to develop is clearly there given the planning reforms included in the recent NPPF. Overall, the construction industry has been relatively resilient in 2024 compared to other industrial sectors. Demand for construction is very much on a domestic level, whereas manufacturing and other industrial sectors are reliant on the global economy.

“From what our clients are telling us, 2025 is expected to be better than last year; however, it’ll be a slow burn. Infrastructure will do well given the government’s investment plans as will commercial as the UK is becoming an investment choice for many. Housing supply will be available but it’s whether demand will follow if interest rates remain stubbornly high.

“While high interest rates and increasing labour costs will continue to have an impact on the industry, an increased flow of inward investment should provide some relief.

“We expect that construction PMI will hover around the same level as it is currently for much of 2025, and any spikes are likely to be short-lived. Although growth will be slow and steady the fundamentals for the sector are solid and there is an air of quiet optimism.”